Somewhere between living and dying, at one time or another, most of us will have a point where we try to pay off the debt we have accumulated along the way. For a lot of folks, this usually comes at a time when you are preparing to buy a house or want to make some space in your budget to save for the future. Credit cards, vehicles and student loans can be a few of the may things we find ourselves owing money for in the grand scheme of things. If you are trying to pay them off in a set amount of reasonable time, it is important to have a plan of attack.

One tool that I have used in the past to pay off accumulated debt is a “snowball” method debt payoff calculator. This is a plan where you can attack your debt with intensity and track results immediately. There are two main recommended methods for using a snowball that are highest to lowest interest, or lowest debt to highest debt.

Method #1 is the highest to lowest interest. In this method, you first must maintain paying a minimum monthly payment on all debt. After the minimums, you must then concentrate the largest part of your excess expendable income into hammering your highest interest debt first (usually consumer or merchant credit cards). The primary reason people would choose this method is to save interest of the period of time in which they want to have everything paid off and be debt free. Many banks have online calculators that allow you to enter information about your debt and will generate visual spreadsheets detailing your payoff structure in a monthly breakdown.

Method #2 is a very popular method and is recommended by expert financial advisor and New York Time’s best-selling author Dave Ramsey. This method ignores interest rates and attacks the smallest debts first. Much in the way people stick with a diet if they see results sooner, this method allows you to see the results of individual debts being paid off quicker for immediate satisfaction. A detailed description of this method can be found at https://www.mytotalmoneymakeover.com/about.

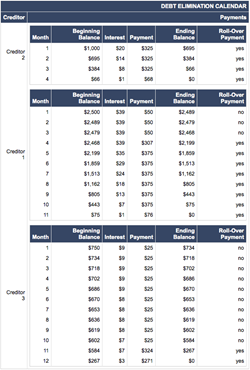

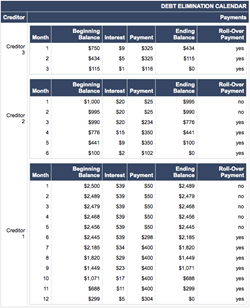

Here are a couple of quick samples I have generated using one of many free online calculators for this type of planning. This setup would allow this person to become debt free in 12 months, so long as no further spending takes place on the debt. They both take on a general assumption that there are three basic creditors with the following information:

- Creditor #1 – Balance of $2500, Minimum monthly payment of $50, Interest rate of 18.9%.

- Creditor #2 – Balance of $1000, Minimum monthly payment of $25, Interest rate of 23.9%

- Creditor #3 – Balance of $750, Minimum monthly payment of $25, Interest rate of 14.9%

- An additional $300 on top of the minimum monthly balance payments available for debt repayment.

| Method #1 |

Method #2 |

|

|

No matter which method you choose, know that you are not alone in your plan to end debt. Many people face the issue of being in debt and it takes motivation and commitment to get ahead of it. In this world of ever-increasing costs of living and not a lot of increased income to compensate for it, it is becoming harder and harder to remain debt-free. Follow a strategized plan of attack, take advantage of all the free online information to combat debt, and you can succeed in your goals to stay afloat in the sea of debt.